The Automation Gap Is Your Window. It's Closing.

By Ben McEachen

Anthropic just quantified the distance between what AI can do and what businesses have actually deployed. That gap is the single most important strategic variable in your business right now.

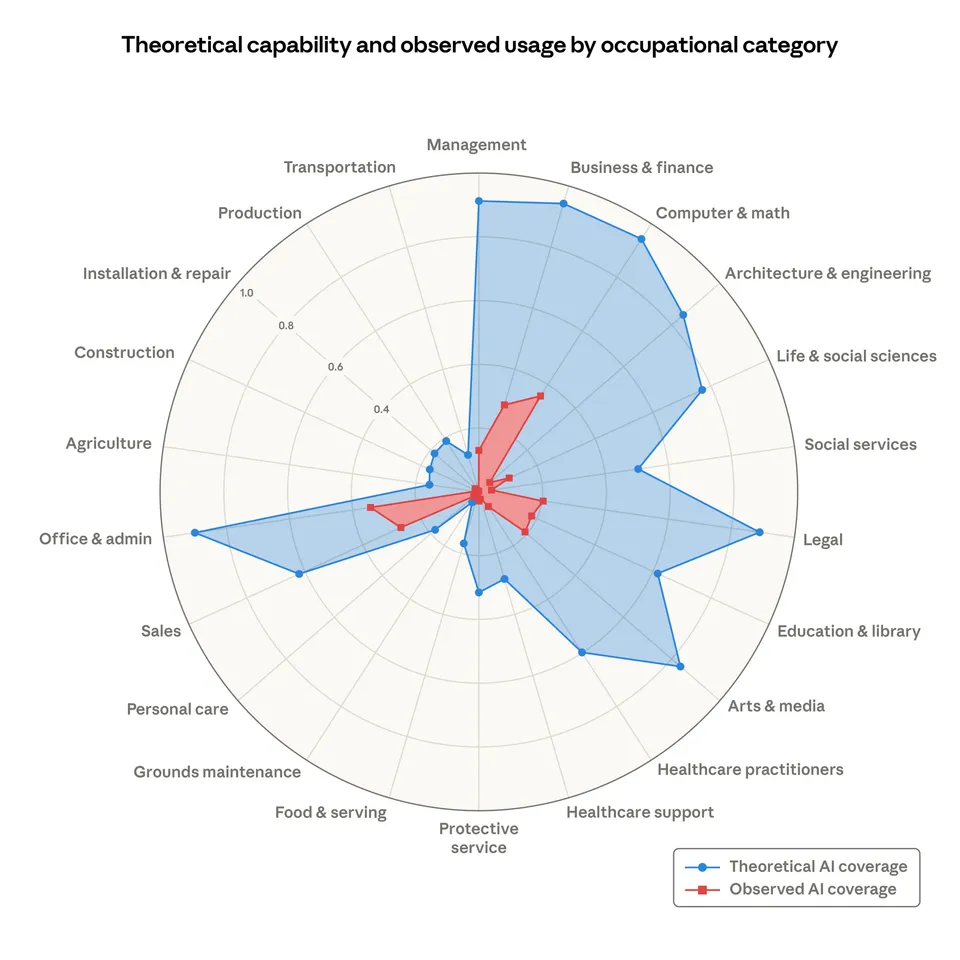

Anthropic published a chart this month that should be taped to the wall of every growing company’s CEO office.

It’s a radar chart. Two colored areas. Blue represents what AI can theoretically do across every major occupational category. Red represents what AI is actually doing today.

The blue dwarfs the red in almost every category.

Computer and math jobs: 94% theoretical capability, 33% actual usage. Legal: 80% theoretical, 15% actual. Business and finance: 95% theoretical, under 40% actual. Office and admin: 90% theoretical, 25% actual.[1]

The distance between blue and red is the single most important strategic variable in your business right now. And you probably don’t know it exists.

A VC looks at that gap and sees a startup opportunity. A founder looks at it and sees a product to build. An operator looks at it and sees something more urgent: a countdown. That gap is your window. It’s the distance between what your competitors could be doing and what they’re doing today. The firms that treat it as breathing room will be the ones who suffocate when it closes. The firms that treat it as a head start will be setting prices and terms when the rest of the market catches up.

The gap isn’t closing uniformly. The automation gap is closing fastest where capital concentrates. The biggest firms close it first, then the pressure works its way down.

What Anthropic Actually Measured

Most AI commentary is speculation dressed up as analysis. This is different.

The Anthropic Economic Index, published in March 2026, introduces something called “observed exposure.” Previous studies measured what AI could theoretically do if fully deployed. Anthropic measured what it’s actually doing, based on real usage data from Claude conversations cross-referenced against the U.S. occupational database (O*NET).[1]

The methodology matters. Tasks that are theoretically automatable only count as “covered” if there’s sufficient real-world professional usage. Fully automated tasks get full weight. Augmentative use (AI assists but doesn’t replace) gets half weight. The result is a radar chart that tells you, in two colors, the distance between possibility and reality.

At the individual occupation level, programmers sit at 74.5% coverage (highest), followed by customer service at 70.1%, market research at 64.8%, sales reps at 62.8%.[1]

Here’s the central finding: AI is nowhere near reaching its theoretical potential. The framework treats the distance between theoretical capability and actual usage as a predictor of future disruption. The larger the gap, the larger the wave still coming. For Computer & Math, that gap is 61 percentage points.

For every 10 percentage point increase in AI coverage, the Bureau of Labor Statistics projects employment growth falls by 0.6 percentage points through 2034.[1] The wave is measurable. And it hasn’t arrived yet for most industries.

The Biggest Firms Close It First

Here’s why this matters if you’re running a company with 30 to 300 employees.

Enterprise adoption is far ahead of you. 92% of Fortune 500 companies use generative AI.[2] 88% of large organizations use AI in at least one business function.[3] Meanwhile, only 39% of U.S. small businesses have adopted AI at all.[4] That number has roughly tripled in a year, but it’s still less than half.

The OECD data makes the size gap stark: 52% of firms with 250+ employees use AI, versus 17.4% of firms with 50-249 employees, versus 11.9% of firms with 10-49 employees.[5] A 35-40 percentage point gap between the top and the middle.

But adoption isn’t the same as maturity. Only about 1% of firms describe themselves as “mature” in AI deployment.[6] 74% of companies have yet to see tangible value.[7] Nearly two-thirds are stuck in pilot stage.[3] The adoption gap is closing. The value extraction gap is wider than ever.

This is where capital matters. Legal tech alone raised $5.99 billion in 2025.[8] Harvey AI hit an $11 billion valuation.[9] Clio hit $5 billion.[10] When capital concentrates at this scale, it builds tools aimed at the verticals where growing companies operate. The tools are coming whether you adopt them or not. Your competitor down the street is the variable.

The gap isn’t closing uniformly. The automation gap is closing fastest where capital concentrates. The biggest firms close it first, then the pressure works its way down.

I’ve seen this pattern in every previous technology cycle: the big firms adopt first, compress their costs, pass some savings to clients, and raise the bar for what “competitive” means. By the time the growing company moves, the early movers have a structural advantage in pricing, speed, and capacity. The gap becomes a moat.

What the Gap Looks Like in Your Industry

Let me get specific. Because the gap isn’t theoretical in your vertical. It’s already visible.

But first, a distinction that matters: when I describe the solutions below, most of them are conventional technology. Databases, rules engines, calendar APIs, document parsing, workflow automation. Standard building blocks. What changed is that AI compressed the cost and speed of building with them. Two years ago, a custom solution for any of these problems would have cost $30K-$50K and taken months. Now it’s viable for a 30-person firm in weeks. AI is sometimes a component inside the tool (pattern matching, synthesis, anomaly detection), but it’s not the whole thing. The “AI does everything” fantasy isn’t what’s actually working. Targeted solutions for specific workflows are.

Legal. The gap is 65 percentage points (80% theoretical, 15% actual). Firms with 51+ attorneys use generative AI at double the rate of solos.[11] Only 26% of family law practitioners have individually adopted AI.[12] What closing the gap actually looks like: imagine you’re looking at 9,000 pages of discovery documents and need to verify that every request got a complete response. A discovery review system built on database logic maps each request to its response, flags gaps and evasive answers, and generates a completeness checklist (AI handles the evasiveness detection; the mapping is conventional tech). A financial disclosure analyzer uses data extraction to surface discrepancies across hundreds of pages of tax returns and account statements. Most of the infrastructure is standard. AI made it affordable to build. I covered this in detail in AI Just Compressed Your Production Costs.

Behavioral health. Group practices, especially telehealth-based, are scaling fast with razor-thin margins. Credentialing with insurance panels takes 90-150 days of paperwork per payer.[13] Billing and claims management is a full-time job at a 10-clinician practice, with denial rates running 5-10% across practices and significantly higher for behavioral health claims specifically.[14] Documentation burden rivals the time spent providing therapy itself.[15] The solutions: automated credentialing status tracking and deadline alerts (database logic, API integrations). Claims submission workflows that flag coding errors before they become denials (rules engines). Templated session note frameworks that reduce documentation time without touching clinical judgment. AI is one layer where appropriate. The backbone is workflow automation. A group practice owner shouldn’t be spending her evenings chasing insurance denials. That’s an infrastructure problem, not a clinical one.

Construction. Sits at the bottom of the chart (15% theoretical, 2% actual), but the gap still matters. Not for the craft, but for the business owner sitting at the desk at 9pm trying to reconcile pay applications. Pay apps in commercial construction involve multiple tiers of documentation, lien waivers, compliance certificates, and approval chains. A project manager spending fifteen hours a week assembling pay applications is doing work that a document parsing system, a compliance checklist engine, and a status tracking database can compress to a fraction of that time. 45% of construction firms report no AI implementation at all. Less than 1% have organization-wide use.[16] The firms that build operational infrastructure for the back office will do 20% more work with the same crews.

Property management. Here’s one that follows a pattern worth noticing: look where the capital is going, then look the other direction. Most investment in real estate AI emphasizes property valuation, pricing models, and market forecasting.[17] The high-profile, data-science-heavy use cases. Meanwhile, the day-to-day operational workflows that actually eat a property manager’s time receive far less attention. Data entry, lease management, financial reconciliation, maintenance coordination. Fewer than half of retail and industrial property operators believe today’s tools meet their needs.[17] Property teams waste five or more hours a week just managing tenant communications, largely because basic comfort issues make up nearly two-thirds of all service requests.[17] AI systems that categorize incoming messages and route maintenance requests to the right vendor offer immediate productivity gains, built on conventional triage logic and rules engines, not the heavy capital lift of deploying fully autonomous chatbots. All the money is chasing market prediction. The efficiency gold mine is in the back office.

Advertising and media agencies. Same pattern, different vertical. Billions in capital investment flowing into media buying and planning automation. But the workflow bleeding money at most agencies isn’t media planning. It’s invoice processing. A global media services team might process over 10,000 vendor invoices manually, a task requiring upwards of 400 man-hours.[18] Reconciliation takes weeks because it requires coordination across vendors, finance, media, and analytics departments. The complexity comes from highly customized deal structures (varying quantities, rates, placements, flighting, targeting) and a complete lack of standardization in digital media invoicing. Digital invoices arrive as a patchwork of non-standardized PDFs, with critical information appearing in completely different places depending on the publisher. The solution is mostly conventional technology: OCR to digitize scanned invoices, matching rules to compare invoices against original media estimates and delivery reports, exception routing that sends discrepancies to a manager’s phone for approval. AI helps with the messy part (parsing non-standardized formats, filling in missing data by scanning seller communications), but the backbone is automation and rules engines. Organizations that have built these systems report processing time reductions of up to 99%.[18] All the capital is chasing the glamorous side of the business. The invoice workflow is where the margin is leaking.

AI changed the economics. Not by doing the work, but by compressing what it costs to build the tools that do the work.

The common thread: in every vertical, the business owner is spending evenings on operational work that should be handled by systems. The large firms have built those systems. Growing companies haven’t, because the economics didn’t justify it. AI changed the economics. Not by doing the work, but by compressing what it costs to build the tools that do the work. And you don’t need a platform that does everything. You need the solution that addresses the specific workflow eating your margins.

Why Growing Companies Stall

If the tools are viable and the gap is real, why haven’t more growing companies moved? Because the obstacles are real too. I hear them in every conversation.

The noise problem. Every AI vendor, consultant, and LinkedIn influencer is telling you to “adopt AI.” The signal-to-noise ratio is terrible. When everything is urgent, nothing is. The CEO who’s heard 40 pitches and read 100 articles is actually less likely to act than the one who heard one clear recommendation from a trusted operator.

The pilot trap. Nearly two-thirds of organizations are stuck in pilot stage.[3] They’ve tried something. It “worked” in a demo. Nobody wired it into the actual workflow. The pilot becomes a checkbox instead of a business decision. 74% of companies have yet to see tangible value from AI initiatives.[7] The problem isn’t the technology. It’s the implementation.

The skills gap. 46% of tech leaders cite AI skill gaps as a major obstacle.[19] But at a 75-person company, that means something different than at a Fortune 500. It means the CEO doesn’t have a CTO, the office manager is the closest thing to an IT department, and nobody has time to evaluate tools while also running the business.

The integration wall. 95% of IT leaders cite integration issues as a primary barrier to AI deployment.[20] At a growing company, “integration” means getting the tool to talk to QuickBooks, the CRM, and the shared drive where everything actually lives.

The cost misconception. This is the one I hear most often. CEOs still think in terms of the old economics: custom software means $30K-$80K, months of development, and a maintenance burden they can’t staff for. That was true two years ago. AI compressed the build cycle. The same solution that would have cost $50K in 2023 can be built in weeks for a fraction of that. But the sticker shock from the old world is still in the CEO’s head. And they’re still thinking in terms of buying platforms, not building targeted solutions for the one or two workflows that actually matter.

These are real constraints. Not excuses. But none of them are permanent. And the companies that figure out how to move past them are the ones creating distance right now.

What Closing the Gap Actually Looks Like

The gap is a window because it represents the distance between what’s possible and what your competitors have done. Today, most of your competitors are in the same position you are: aware of AI, unsure how to act, stuck in pilots or doing nothing. That won’t last. The capital flowing into every vertical is building tools that will make adoption easy enough for the laggards. When that happens, the early movers have already restructured.

Here’s what the early movers are doing.

Building only what they need, not buying platforms they don’t. They’re identifying the one or two workflows that are actually bottlenecking growth and building precisely for those. A behavioral health practice that automates its credentialing workflow. A construction firm that cuts fifteen hours a week of pay app assembly down to a fraction. A media agency that processes 10,000 invoices without 400 man-hours of manual reconciliation. A property management company that routes maintenance requests to the right vendor in seconds instead of losing five hours a week to email triage. A law firm that reviews 9,000 pages of discovery for completeness in hours instead of days. These aren’t AI-powered fantasies. They’re database logic, document parsing, calendar APIs, and workflow automation, built in weeks instead of months because AI compressed the development cycle. The tools are polished, specific to the business, and maintainable. And because you’re only building the parts that matter, there’s no shelfware, no six-month implementation, no features nobody asked for.

Restructuring pricing around the new cost structure. The firms that benefit from the gap aren’t just faster. They’re repricing their services. In legal, that means flat fees instead of hourly billing. In property management, it means managing more units without adding headcount. In construction, it means tighter bids because the back-office overhead dropped. The tool is a cost input. The pricing decision is the business model move.

Treating implementation as an operational project, not a technology project. The pilot trap exists because companies treat this as a technology initiative: evaluate tools, run a pilot, present results. The early movers treat it as an operational project: identify the highest-leverage workflow (the one where a small improvement compounds across the business), build the solution, measure the business outcome, then move to the next one. That sequencing decision, which workflow first, how fast, what to skip entirely, is a strategy call, not a technology call. Technology projects get owned by IT. Operational projects get owned by someone who understands the business. That’s what fractional COO work looks like in practice.

The Chart on the Wall

Print that radar chart. Put it on your wall. Not because it predicts which jobs AI will replace. It doesn’t. Put it up because it shows you, in two colors, the distance between what’s possible and what’s been done.

That gap is a business model decision. Every vertical has its own version of it. Legal, behavioral health, construction, property management, advertising. The specifics change. The shape of the opportunity doesn’t.

The gap is closing. It’s closing fastest where capital concentrates, with the biggest firms moving first and the pressure working its way down. The firms that move first aren’t the ones with the best technology. They’re the ones that understood the gap was a window, not a moat.

The window doesn’t close all at once. It closes the way Hemingway described going bankrupt: gradually, then suddenly. The “gradually” part is now. The “suddenly” part is when the tools get easy enough that your competitor down the street starts using them without thinking about it. By then, the early movers have already restructured.

The question isn’t whether your business will change. The question is whether you build the infrastructure first or your competitor does.

If you’re running a growing company and this resonated, I’d like to hear what operational problem is eating your evenings. Here’s how fractional COO work fits growing companies, or just get in touch.

Next in this series: 30% of American workers have zero AI exposure. The entire industry is building for the wrong people.

References

[1] Anthropic Economic Index, March 2026 · [2] OpenAI Fortune 500 adoption, Aug 2024 · [3] McKinsey, “The State of AI in 2025” · [4] Thryv, “AI and Small Businesses Survey,” 2024 · [5] OECD, “AI Adoption by SMEs,” Dec 2025 · [6] SmartDev, AI maturity benchmark, 2025 · [7] BCG, “Where’s the Value in AI?” Oct 2024 · [8] Artificial Lawyer, Legal Tech Investment 2025 · [9] TechCrunch, Harvey AI valuation, Feb 2026 · [10] JD Journal, Clio valuation, Nov 2025 · [11] Clio, “Legal Trends Report 2025” · [12] ABA, “Legal Industry Report 2025” · [13] CAQH credentialing timelines · [14] MGMA, claim denial benchmarking · [15] Eleos Health, documentation burden research · [16] RICS, AI in construction survey, 2025 · [17] JLL / OECD real estate technology surveys · [18] AutomationEdge, media invoice processing · [19] TechRepublic, “AI Adoption Trends 2026” · [20] MuleSoft/Salesforce, “2025 Connectivity Benchmark”